Brief Guide to Learn: How Is Total Loss Value Calculated?

Oct 12, 2023 By Susan Kelly

Introduction

Value after Total Loss - How Is It Determined? There were a total of 312,988 car accidents involving Illinois drivers in 2019. Eighty-nine thousand one hundred thirty-three people were injured, and 1,010 lost their lives due to these accidents. More than ten individuals are hurt every hour due to car crashes. When something as serious as an accident occurs, it's a pain to deal with insurance companies incentivized to pay you less than your car is worth. Understanding how insurance companies arrive at their total loss valuation is crucial before accepting any offer they provide. This article will go over how auto insurance firms in Illinois figure out payouts in the event of a totaled vehicle and what you can do to ensure you get your fair share.

Calculating Total Loss Value

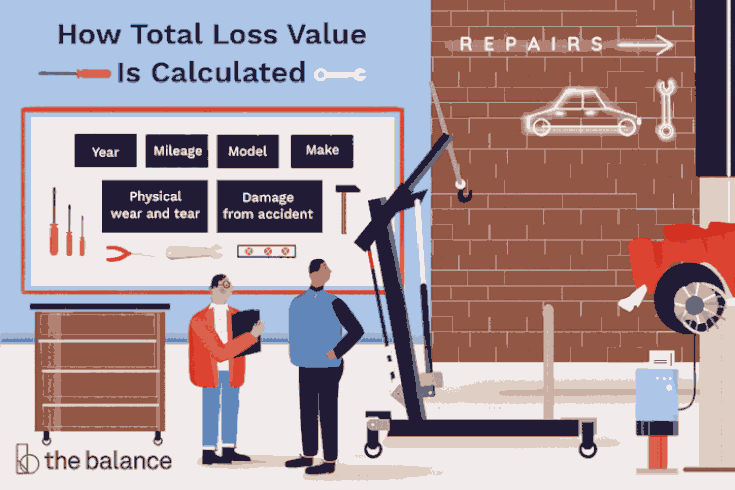

Numerous factors determine the Total Loss and the Actual Cash Value. Here's how it operates:

- The company will send an "adjuster" to examine the car's exterior and engine to determine if repairs are necessary and how much they would cost.

Following the inspection, a determination is made as to the vehicle's "Actual Cash Value" by considering factors such as:

- Amount of depreciation

- Date of manufacture

- Model

- Manufacturer

- Age

- Mileage

- Wear and Tear of the current state of the automobile market.

The value was based on an appraisal of the car's condition before the accident. When the damage exceeds fifty percent of its value, it is considered a total loss (in most circumstances).

Total Loss Claims and Actual Cash Value

It would help if you had property damage liability (PD) or comprehensive or collision coverage to get a payout for a totaled vehicle. PD is required in every state, but the only method to collect on it is to claim another driver's policy. You can seek compensation from PD only if you can prove that the other driver was also at fault for the collision. Collision insurance is the quickest and most reliable way to collect money for a totaled car from your insurance carrier.

No of who was at fault in a collision, the policyholder is still responsible for the deductible before the insurer pays anything. Assuming you have the appropriate insurance in place (and are not injured or otherwise preoccupied), your first order of business should be to file a claim with your insurer once the damage has occurred. An insurance adjuster will visit you to evaluate the damage to your vehicle. Here is where the declaration of total loss will be made.

Cars Depreciate in Value

As soon as you drive off the lot in your brand-new car, its value starts to drop, and it stays there for as long as you own it. On average, an automobile loses 20% of its value in the first year and another 40% in the subsequent four years. 3 A negative equity situation arises when the value of your vehicle drops below the amount still owed on your auto loan. When buying a car, selecting the shortest loan term is important to prevent financial trouble due to being upside down on payments. You may speed up the process of accumulating wealth this way.

You Don't Have Gap Insurance

The difference between what you owe on your car and its current value can be substantial. This insurance is a must for some loan providers but is not required by others. The gap between your insurance payout and auto loan debt is your financial responsibility if you do not have gap insurance.

Which Claim Category Does Total Loss/Constructive Total Loss Fall Under?

Own Damage (OD) is a type of claim that covers the full cost of the loss or the cost to rebuild. The Own Damage plan will reimburse you for any financial losses you sustain in the event of an accident, natural or artificial disaster, fire, explosion, or total loss. Both the OD plan and the Third-Party Liability Plan are included in the All-Inclusive Motor Insurance Policy. Only if you have the Comprehensive Plan may you file a claim under Own damage for damages to your car that are beyond repair. Additional coverage can be added to your Comprehensive Plan by selecting one of the optional policy riders.

Conclusion

If the repair cost exceeds its current market worth or a certain proportion of its value, your insurance provider may declare your vehicle a total loss. You will be responsible for the difference if your total-loss compensation is less than the amount still owed on your car loan. Making smart choices when applying for a car loan will help you avoid financial difficulty in the event of a totaled vehicle.